First announced in October 2017, Beem It is a peer-to-peer payments app owned by Commonwealth Bank (CBA), National Australia Bank (NAB), and Westpac.

It enables users with Visa or Mastercard debit cards to send, request, split, and receive payments (reportedly within 10 seconds) and is not restricted to the major banks’ customers. Beem It has a limit of $200 per day for sending money and $10,000 for receiving money.

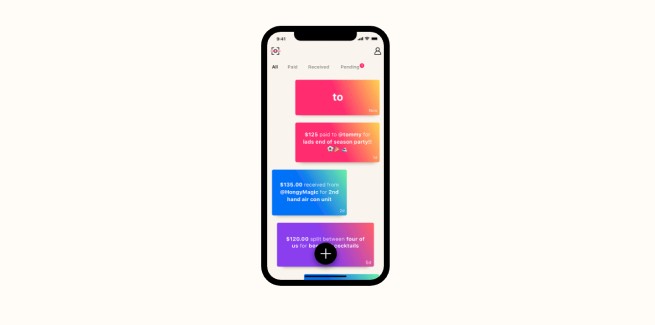

The app has social media-esque vibes as the interface looks like a text messaging platform, allowing users to choose their username and add any type of payment description (which can even be adorned with emojis). Users can also see which people in their contacts list are using Beem It.

However, the service won’t function unless all parties have the app installed.

The app is currently free to use, but the major banks’ intention is to monetise it eventually.

The launch of the app follows the Australian Competition and Consumer Commission (ACCC) denying authorisation to the CBA, NAB, Westpac, and Bendigo and Adelaide Bank to act as a cartel when negotiating with Apple to open up access to its iPhone’s Near-Field Communications (NFC) chip. The access would have enabled the major banks’ own mobile banking applications to support contactless payments over NFC.

The tech giant argued against opening up access to its NFC chip as it would “undermine” the availability, security, and privacy its customers expect when making payments using Apple devices.

While ANZ has not clarified why it is not part of the joint venture, the bank is the only one of the big four to have adopted Apple Pay, along with Google Pay (formerly Android Pay), Fitbit Pay, Garmin Pay, and Samsung Pay, in addition to its own ANZ Mobile Pay platform.

CBA, NAB, and Westpac allow customers to pay via other mobile platforms, except for Apple Pay.

Earlier this year, Australia’s New Payments Platform (NPP) was launched, facilitating instant, cross-institutional transfer of funds.

NPP Australia, the organisation established to oversee the development and operation of the platform, said in February that within a year of the platform's launch, businesses will also be able to send payment requests to customers with payment information included.

The NPP also offers more room to outline what payments are; instead of just 18 characters, the platform will allow for a 280-character transaction description.

However, the managing director of Australia Invoice Finance, Greg Charlwood, noted that the reduced transaction time could lead to more fraudulent banking activity, as experienced in the UK and Singapore after the launch of their real-time payments platforms.

“Under the NPP, financial institutions will no longer have one or two days to detect and stop fraudulent transactions as they currently do. Real-time transfers of funds mean they will need to become more vigilant around the prevention of fraud rather than reacting to fraudulent transactions,” Mr Charlwood said.

[Related: Major banks apologise for technology faults]